UAE CT will be applicable across all Emirates and will apply to all business and commercial activities alike, except for the extraction of natural resources, which will continue to be subject to Emirate level taxation.

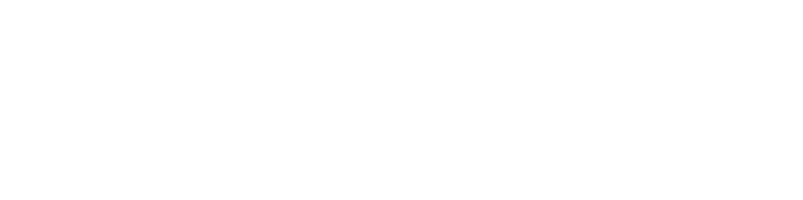

UAE CT will be applicable at the following rates:

| Taxable income | UAE CT rate |

|---|---|

| AED 0 - AED 375,000 | 0% |

| Above AED 375,000 | 9% |

Free zone businesses will be within the scope of UAE CT and required to register and file a CT return, but will continue to benefit from CT holidays / 0% taxation if they comply with all regulatory requirements and do not conduct business with mainland UAE.

The press release and FAQs indicate that there will be a different tax rate for large multinationals that meet the criteria under ‘Pillar Two’ of the OECD Base Erosion and Profit Shifting project (i.e. that have consolidated global revenues above EUR 750m).

CT will be payable on the accounting net profit reported in the financial statements of the business, with minimal exceptions and adjustments. Tax losses incurred from the CT effective date can be carried forward to offset taxable income in future financial periods.

No UAE CT will apply to:

- Employment income, income from real estate, income from savings, investment returns and other income earned by individuals in their personal capacity that is not attributable to a UAE trade or business;

- Dividends, capital gains and other investment returns earned by foreign investors.

Exemption from UAE CT will be available for:

- Capital gains and dividends earned from qualifying shareholdings;

- Qualifying intra-group transactions and restructurings.

Domestic and cross border payments of interest, dividends, royalties and other payments will not attract a withholding tax in the UAE, and foreign tax credits will be available for taxation incurred by UAE businesses on income earned outside the UAE.

UAE CT will have to be filed electronically once for each financial period without a requirement for advance UAE CT payments on the basis of provisional tax returns.

UAE group companies can form a tax group and file a single tax return for the entire group, and transfer tax losses to other members of the group.

The UAE CT regime will have transfer pricing rules and documentation requirements in line with the OECD Transfer Pricing Guidelines.

The Federal Tax Authority will be responsible for the administration, collection, and enforcement of CT.